15 Common EBITDA Add-Backs to Maximize Sale Price

15 Common EBITDA Add-Backs to Maximize Sale Price In early 2026, securing a premium enterprise valuation requires sell-side advisors to locate and defend every valid adjustments. Picture an advisor representing a software development firm in Ohio. The advisor packaged the transaction using raw G

15 Common EBITDA Add-Backs to Maximize Sale Price

In early 2026, securing a premium enterprise valuation requires sell-side advisors to locate and defend every valid adjustments. Picture an advisor representing a software development firm in Ohio. The advisor packaged the transaction using raw GAAP accounting figures, showing an EBITDA of $2.2 million. During diligence, the strategic buyer noticed that the seller had failed to add back one-time restructuring costs and owner automobile expenses. Because these adjustments were omitted, the buyer applied their multiple to the lower baseline, costing the seller $1.4 million in transaction proceeds.

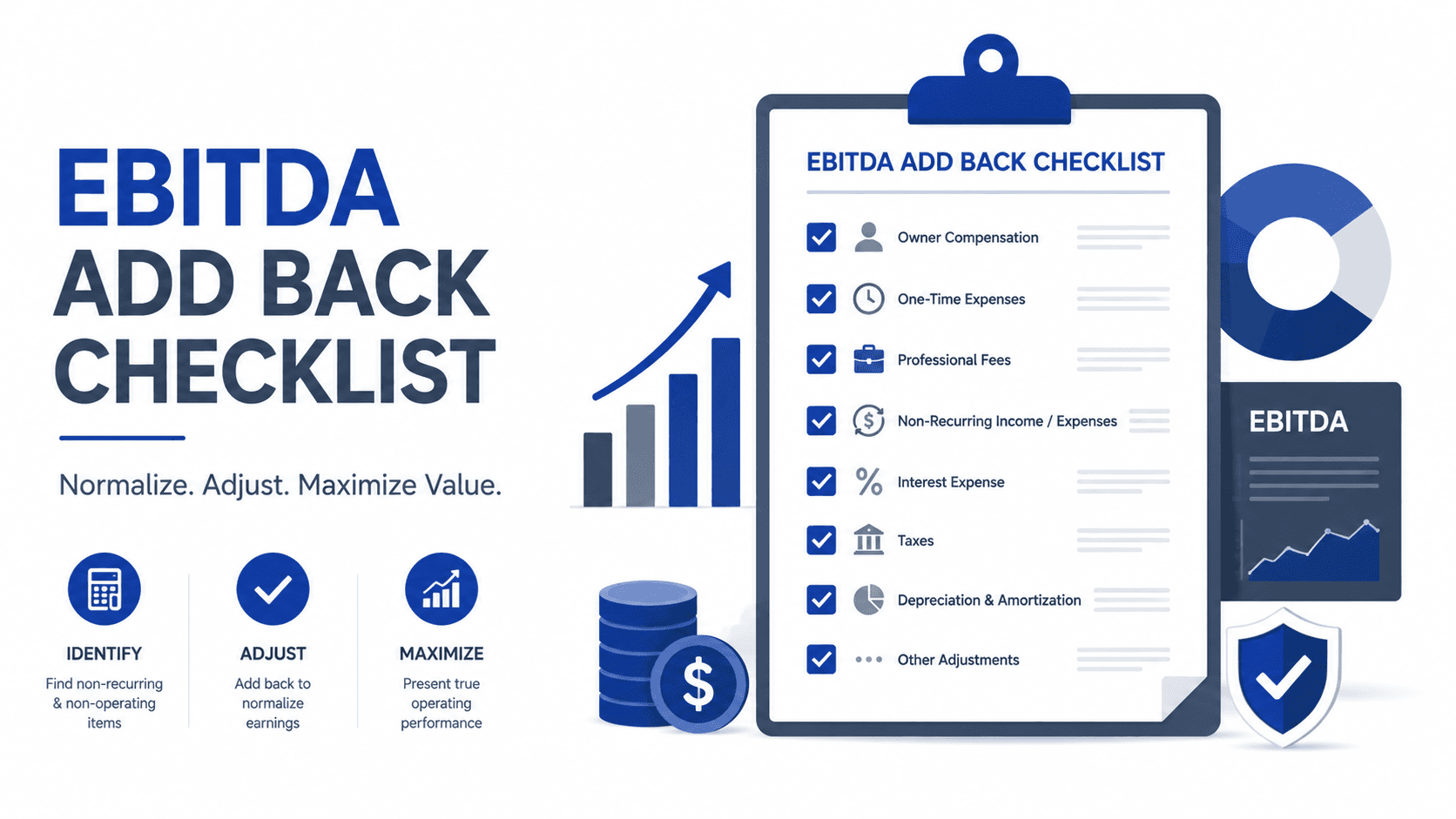

To capture maximum value, sell-side teams must use a comprehensive ebitda add back checklist during deal preparation. Utilizing our interactive EBITDA normalization calculator tool helps transaction teams identify discretionary and non-recurring expenses. Documenting these adjustments ensures that the business is priced on its true recurring earnings.

Free Resource: Map your normalization adjustments and calculate a defensible EBITDA bridge with our interactive EBITDA normalization calculator tool.

Why an EBITDA Add-Back Checklist is Essential for Sellers in 2026

Under transaction disclosure guidelines monitored by the Securities and Exchange Commission (SEC), buyers must analyze purchase price allocations and underlying earnings. For private sellers, historical financial statements reflect tax-minimization strategies rather than economic reality. Private owners often run personal expenses, related-party transactions, and above-market executive pay through corporate accounts, which lowers reported profits.

Under the regulations of the Internal Revenue Service (IRS), these transactions are tax-deductible. However, in an M&A context, these expenses will not transfer to the buyer. Reversing these expenses is essential to showing the recurring earning power of the target.

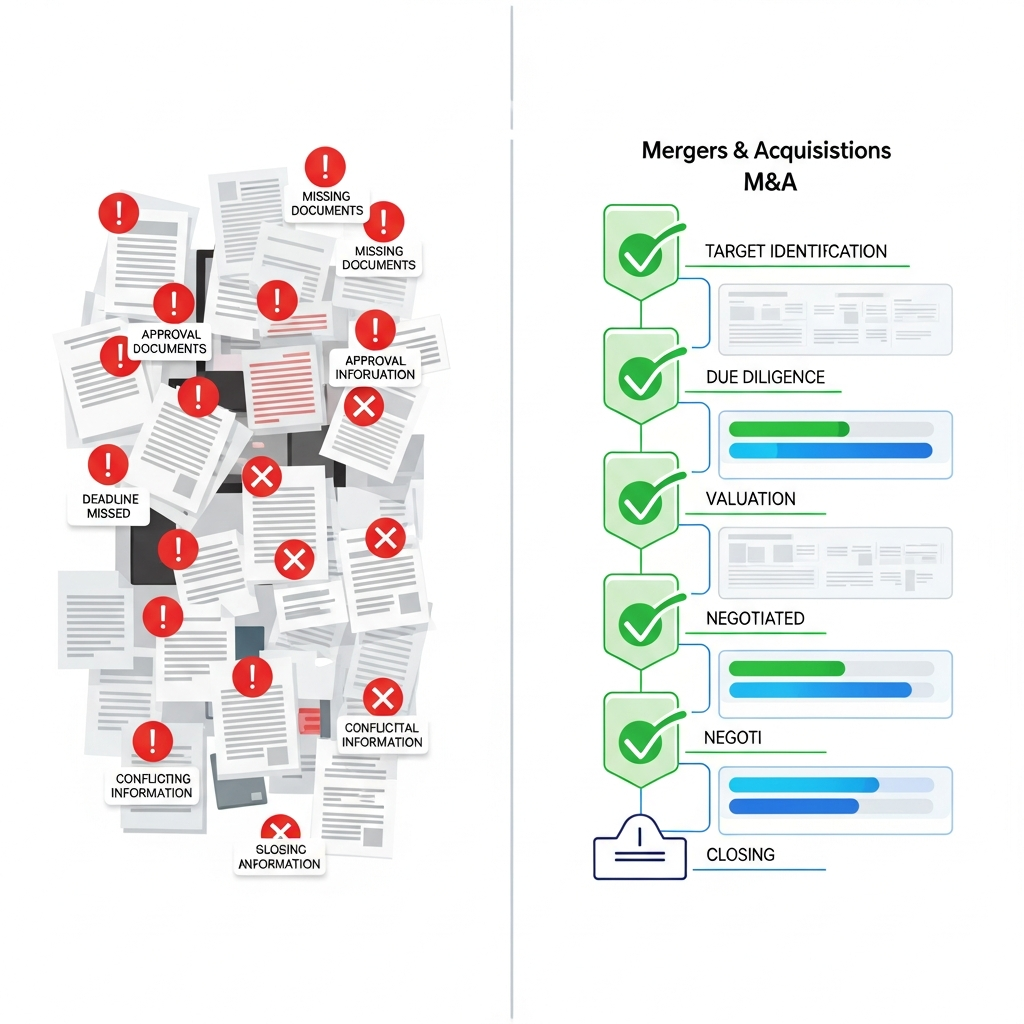

Case Studies: The Financial Impact of Add-Back Defense

Real-world transaction outcomes highlight the importance of structured add-back adjustments.

Case Study: The Forgotten Software Integration Write-off

Problem: A boutique advisory firm in the Midwest represented a logistics firm. The analyst used reported EBITDA of $2.5 million, forgetting to add back $180,000 in one-time software integration fees.

Action: The buyer’s financial team accepted the reported $2.5 million baseline, applying a 6.0x multiple to structure their purchase offer.

Result: The failure to add back the non-recurring software fee reduced the purchase price by $1.08 million. The transaction closed before the seller identified the error.

How It Should Be Done: Structured Add-Back Reconciliation

Problem: A medical services company in the Southeast sought a strategic acquisition. The owner paid himself an above-market salary of $420,000 and personal travel out of corporate accounts.

Action: The sell-side advisor identified $220,000 in excess owner salary and $80,000 in personal travel perks, building a detailed add-back bridge.

Result: The advisor presented a normalized EBITDA that was $300,000 higher than reported. The buyer accepted the defensible bridge, allowing the seller to secure a premium valuation.

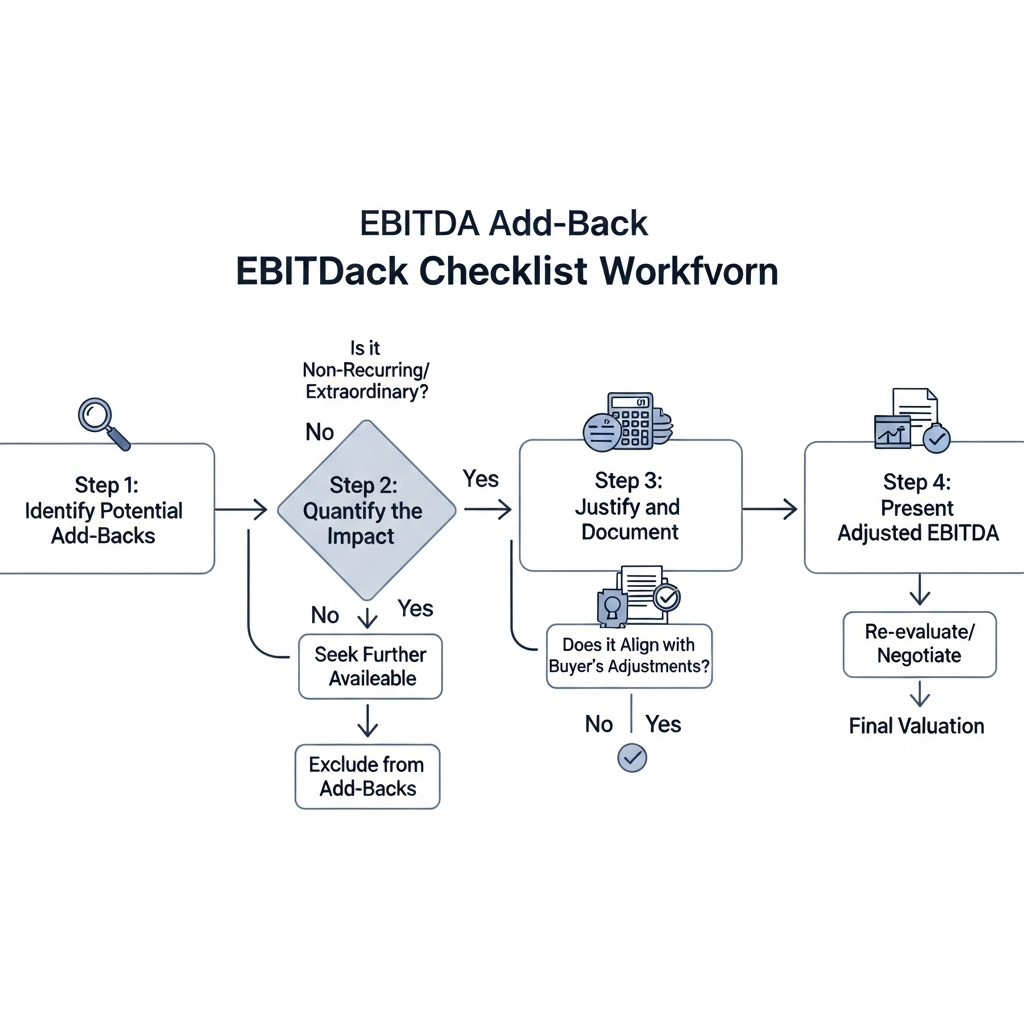

Operational Checklist for Identifying and Defending EBITDA Add-Backs

Deal teams should use this operational checklist to locate and defend valid EBITDA adjustments.

Phase 1: Auditing Executive Compensation and Discretionary Benefits

- Verify Owner Salaries: Compare active owner compensation with market replacement rates to identify adjustments.

- Review Family Payroll: Locate family members on the payroll who do not perform active corporate roles.

- Isolate Owner Perks: Identify vehicle leases, club memberships, and personal travel expenses paid by the firm.

⚠️ Common Mistake: Claiming owner compensation add-backs without providing W-2 records or employment contracts.

Phase 2: Isolating One-Time Operating and Legal Expenditures

- Audit Legal Costs: Separate ongoing corporate legal fees from one-time litigation or settlement costs.

- Review IT Upgrades: Group one-time software migration or ERP system installation fees as non-recurring adjustments.

- Check Facility Relocations: Isolate warehouse moving costs, lease termination fees, and setup costs.

⚠️ Common Mistake: Treating ongoing software licensing fees or routine maintenance as one-time add-backs.

Phase 3: Adjusting for Facility and Operational Leases

- Review Related-Party Rent: Compare rent paid to owner-controlled real estate entities with local market rates.

- Identify Idle Capital: Locate leases for equipment or vehicles that are no longer active in core operations.

- Adjust Lease Terms: Isolate the impact of above-market lease structures that will be terminated post-closing.

⚠️ Common Mistake: Adjusting related-party rent rates without providing local real estate appraisal data.

Phase 4: Documenting and Proving Each Adjustment to Buyers

- Compile Invoice Files: Collect all invoices, bills, and contracts that prove each claimed add-back.

- Build Reconciliation Bridges: Create a clear table showing the calculation from reported GAAP income to normalized EBITDA.

- Draft Explanatory Notes: Write a paragraph for each adjustment to explain the business reason for the add-back.

⚠️ Common Mistake: Listing adjustments in the CIM without compiling the supporting document files.

Allowable M&A Add-Backs vs. Disallowed Personal Adjustments

Allowable Add-Backs

- Discretionary Perks: Personal vehicle leases, country club dues, and family travel paid by the firm.

- Owner Compensation: The portion of the owner’s salary that exceeds market-rate replacement costs.

- One-Time Costs: Litigation settlements, IT system overhauls, and facility relocation costs.

Disallowed Adjustments

- Routine CapEx: Ongoing maintenance costs for plant equipment and basic office software.

- Normal Legal Fees: Standard legal expenses for contract reviews and corporate compliance.

- Normal Salary Increases: Standard payroll increases for key employees who are staying with the business.

EBITDA Add-Back Benchmarks by Deal Size in 2026

We have summarized standard add-back allowances below to support transaction modeling.

Lower-Middle Market Transactions

Deals under $15 million average add-back adjustments of 12% to 20% of reported EBITDA, driven by discretionary owner spending.

Mid-Market Transactions

Transactions in the $15 million to $50 million range average adjustments of 8% to 15%, focused on non-recurring IT overhauls.

SaaS and Tech-Enabled Sectors

Software acquisitions average add-backs of 10% to 18% of revenues, driven by capitalized development and restructuring.

Manufacturing and Industrial Sectors

Manufacturing transactions average adjustments of 6% to 12% of margins, focused on environmental upgrades and related-party rent.

Using Modern Advisory Software to Protect Your Valuation Adjustments

Boutique investment banks often spend hours compiling financial adjustments in spreadsheets. By utilizing our AI CIM packaging suite, advisory teams can convert bookkeeping data into professional transaction materials.

In addition, our VDR Kanban workflow helps advisors organize tax documents, payroll logs, and valuation benchmarks. This organization speeds up buyer due diligence and prevents re-trading. Advisors can verify their calculations by using our EBITDA normalization calculator tool to ensure their valuations remain defensible.

Frequently Asked Questions

What is an EBITDA add-back and how does it impact valuation?

An EBITDA add-back is an adjustment that adds non-recurring or discretionary expenses back to earnings, which increases the valuation baseline.

What are the most common executive perks added back in M&A?

Common perks include corporate auto leases, personal travel expenses, club dues, and family members on the payroll without active roles.

Why do buyers challenge non-recurring legal expenses?

Buyers audit legal add-backs to ensure the costs are truly one-time, rather than ongoing expenses related to routine compliance or patent protection.

How does customer concentration impact add-back validity?

High client concentration increases overall deal risk, making buyers more likely to challenge adjustments to ensure cash flows are stable.

How does an EBITDA normalization calculator support sell-side packaging?

A calculator automates the adjustment math, applying standard category parameters to output a defensible normalized EBITDA schedule.

Disclaimer: The financial and legal information provided in this article does not, and is not intended to, constitute professional legal or financial advice; instead, all information, content, and materials available on this site are for general informational purposes only. Readers should contact their legal counsel or certified public accountant to obtain advice with respect to any particular transaction or regulatory matter.

Ready to automate M&A drafting & secure transaction readiness?

AIVI empowers boutique M&A firms and investment banks to generate CIMs, conduct instant VDR gap checks, and manage exit readiness automatically from a unified data model.