5 Common Discount Rate Mistakes in Small Business Valuation (Errors)

5 Common Discount Rate Mistakes in Small Business Valuation (Errors) In early 2026, establishing a defensible valuation baseline requires absolute financial precision. Picture a business broker in Los Angeles presenting a Discounted Cash Flow (DCF) model to a private equity buyer. The broker cla

5 Common Discount Rate Mistakes in Small Business Valuation (Errors)

In early 2026, establishing a defensible valuation baseline requires absolute financial precision. Picture a business broker in Los Angeles presenting a Discounted Cash Flow (DCF) model to a private equity buyer. The broker claimed a high enterprise value by applying an arbitrary 10% discount rate. The buyer's analytical team quickly flagged that the rate failed to account for the company's size risk and current debt costs. The transaction collapsed during preliminary negotiations because the discount rate calculations lacked market-backed evidence.

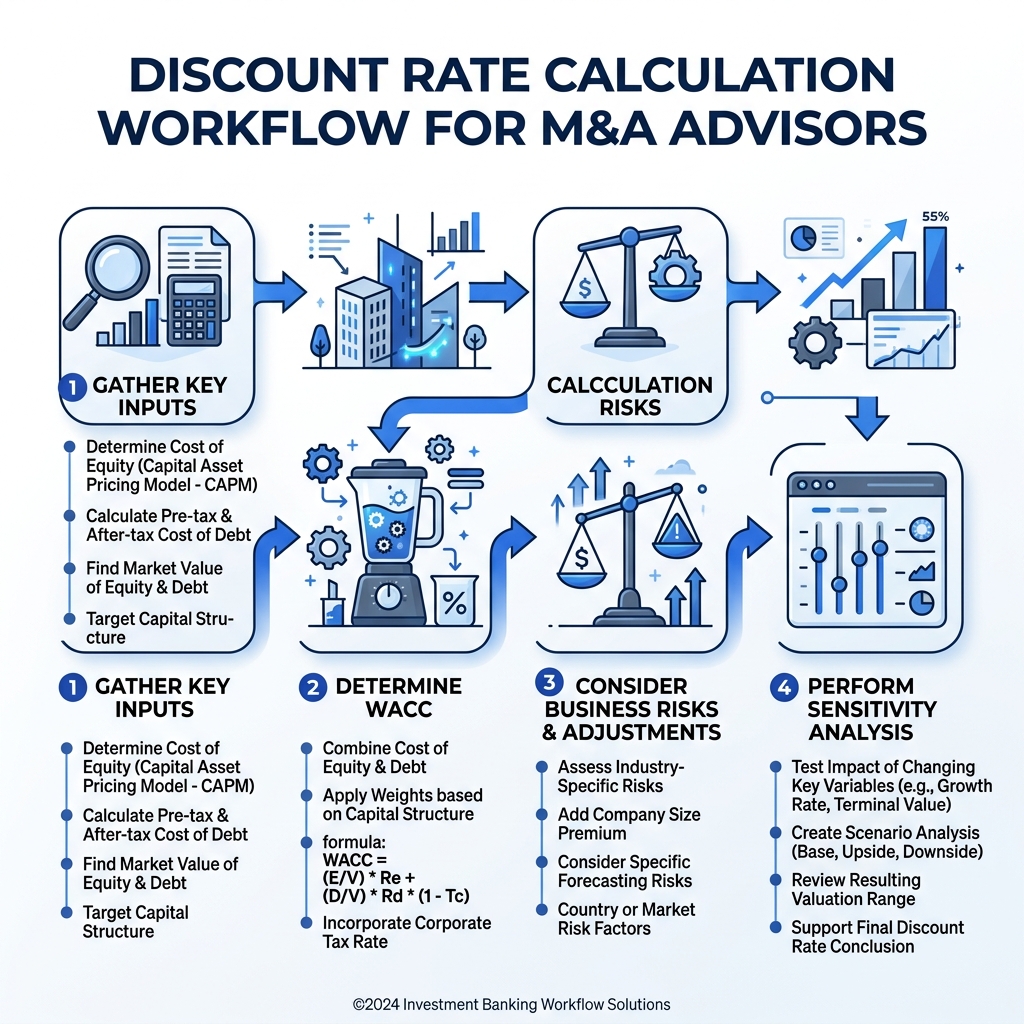

To maintain transaction momentum, sell-side advisors must understand how to calculate defensible discount rates. The Weighted Average Cost of Capital (WACC) model is the standard method used to size discount rates. Before presenting to institutional buyers, sell-side teams should focus on estimating your discount rate using our interactive WACC calculator to verify their baseline assumptions.

Free Resource: Model defensible WACC calculations and audit your discount rate assumptions with our interactive WACC calculator.

Why Discount Rates are Miscalculated in Small Business Valuation

Under the current credit guidelines compiled by the Small Business Administration (SBA), borrowing costs for private acquisitions have experienced volatility. Because debt financing has become more expensive, the cost of debt has a massive impact on the overall WACC. Buyers can no longer assume low-interest debt packages to boost equity returns, which directly impacts the discount rate applied to future cash flows.

This guide outlines how to determine these variables.

Case Studies: The Costly Impact of Discount Rate Mistakes

Examining recent transaction outcomes shows the consequences of using an unverified WACC calculation.

Case Study: The Mismatched Public Comp Error

Problem: A boutique advisory firm in the Northeast represented a specialty logistics business with $20 million in revenue and $3 million in EBITDA. The analyst used a flat, arbitrary 9% discount rate without building a formal WACC bridge.

Action: The buyer's financial team audited the model during confirmatory diligence. They showed that when accounting for the company’s small scale and current cost of debt, the correct discount rate was 13.5%.

Result: The buyer re-calculated the DCF, which reduced the target enterprise value by over $4 million. The seller refused the reduction, and the transaction collapsed.

How It Should Be Done: Structured WACC Defensibility

Problem: A boutique HVAC manufacturer in the Midwest faced buyer due diligence during a strategic sale.

Action: The advisor built a WACC model. The analyst calculated the cost of equity by taking the risk-free rate, adding an industry-specific beta, and adding a 3.5% size premium to account for the company's middle-market scale.

Result: By presenting a detailed WACC bridge showing a defensible 12.2% discount rate, the advisor defended a realistic enterprise value range. The strategic buyer accepted the baseline, and the deal closed on schedule.

5 Common Discount Rate Valuation Errors and How to Fix Them

To execute a defensible valuation process, advisors and owners must avoid these five critical discount rate mistakes.

Error 1: Ignoring Private Company Size Premiums

- Calculate Scale Difference: Evaluate how much smaller the target company is compared to publicly traded peers.

- Apply Size Premium: Add a standard size premium (typically 2.0% to 4.5%) to the cost of equity calculation to reflect higher small-company risk.

- Verify Valuation Baseline: Ensure the resulting discount rate is adjusted upward to prevent inflating the business value.

⚠️ Common Mistake: Treating a small business as if it carries the same operational risk as a multi-billion dollar public corporation.

Error 2: Miscalculating the After-Tax Cost of Debt

- Locate Current Interest Rates: Identify the actual interest rates paid on the firm's active loans, rather than historical coupon rates.

- Apply Marginal Tax Rate: Adjust the interest rate downward by multiplying by (1 minus the marginal corporate tax rate).

- Incorporate Tax Shield: Reconcile the interest tax shield in the WACC formula to show the true cost of debt capital.

⚠️ Common Mistake: Using pre-tax interest rates in WACC, which ignores the tax deductibility of interest and overstates the discount rate.

Error 3: Using Mismatched Public Group Betas

- Select Operational Peers: Identify public peers that share the target's specific business model and customer types.

- Unlever the Peer Betas: Strip out the capital structure differences from the public peer betas to calculate asset risk.

- Re-lever for Target Structure: Adjust the baseline beta to reflect the target company's debt-to-equity ratio.

⚠️ Common Mistake: Pulling raw public betas from a financial portal and applying them directly to a private company without adjusting for leverage.

Error 4: Overlooking Key-Man and Concentration Risk Premiums

- Audit Customer Revenue: Check if any single client represents more than 15% of the firm's revenue.

- Quantify Key-Man Dependency: Evaluate how much business depends on the active presence of the current owner.

- Add Company Risk Premium: Increase the discount rate by a company-specific risk premium (1% to 3%) to reflect these key risks.

⚠️ Common Mistake: Assuming standard industry risk parameters fit a business with high customer or management concentration.

Error 5: Failing to Run Sensitivity Analyses for Discount Rates

- Build a Sensitivity Grid: Create a table showing the enterprise value at different discount rate intervals (e.g., in 0.5% increments).

- Verify Cash Flow Projections: Test how sensitive future capital investment plans are to changes in financing costs.

- Present Range to Acquirers: Offer potential buyers a structured valuation range rather than a single number.

⚠️ Common Mistake: Presenting a static DCF model, which makes the valuation look unrealistic and vulnerable to credit changes.

Cost of Equity vs. Cost of Debt in Small Firm Valuations

Cost of Equity (Ke)

- Calculation Basis: Calculated using risk-free treasury yields plus public peer betas and size risk premiums.

- Capital Priority: Paid last in the event of bankruptcy, representing the highest risk capital.

- Relative Cost: Typically higher than debt costs, ranging from 12% to 18% for private mid-market firms in 2026.

Cost of Debt (Kd)

- Calculation Basis: Based on current bank interest rates adjusted downward for corporate tax shields.

- Capital Priority: Paid first in liquidation, presenting lower risk to capital providers.

- Relative Cost: Typically lower than equity costs, ranging from 6% to 9% depending on collateral and leverage.

Key WACC Parameter Benchmarks in 2026

To help advisors navigate WACC metrics without relying on rigid tables that cause layout issues on mobile devices, we have summarized the current 2026 benchmarks.

Risk-Free Baseline Rate

The risk-free rate is benchmarked against 10-year U.S. Treasury yields, serving as the foundation before adding equity risk premiums.

Average Control Mezzanine Rates

Mezzanine debt costs range between 8.5% and 11.0% in the current market, depending on cash flow coverage.

Typical Private Size Premium Calibration

Valuation analysts calibrate private size premiums between 2.0% and 4.5% depending on EBITDA scale.

Corporate Marginal Tax Calibration

Advisors use a standard marginal tax rate of 21% to 26% to calculate after-tax cost of debt.

How AIVI Streamlines Valuation and CIM Workflows for Advisors

Boutique M&A advisory teams spend dozens of hours manually formatting spreadsheets. By leveraging our automated CIM generator, advisors transform financial models into polished presentations.

The platform links WACC calculations directly with marketing materials, ensuring that DCF projections remain consistent. Advisors can also identify premium strategic buyers by accessing estimating your discount rate using our interactive WACC calculator to verify their baseline assumptions.

Frequently Asked Questions

Why is the discount rate so critical in business valuation?

The discount rate determines the present value of cash flows. A small increase (e.g., from 10% to 11.5%) can reduce value by hundreds of thousands of dollars.

How does the size premium affect WACC for small businesses?

Analysts add a size premium (2.0% to 4.5%) to the cost of equity to reflect small business risks, which increases the WACC and lowers the valuation.

What happens if a valuation ignores the tax shield on debt?

If a valuation ignores the tax shield, it uses pre-tax debt costs. This overstates WACC, artificially depressing present value.

How do advisors calculate company-specific risk premiums?

Advisors evaluate client concentration, key-man risk, and technical barriers, adding a premium (1.0% to 3.0%) based on these risks.

Why should M&A teams avoid using an arbitrary 10% discount rate?

A flat 10% rate ignores current market credit conditions, company size, and debt structures. Institutional buyers reject valuations not backed by market data.

Disclaimer: The financial and legal information provided in this article does not, and is not intended to, constitute professional legal or financial advice; instead, all information, content, and materials available on this site are for general informational purposes only. Readers should contact their legal counsel or certified public accountant to obtain advice with respect to any particular transaction or regulatory matter.

Ready to automate M&A drafting & secure transaction readiness?

AIVI empowers boutique M&A firms and investment banks to generate CIMs, conduct instant VDR gap checks, and manage exit readiness automatically from a unified data model.