Accounting for Seasonal Working Capital Adjustments in M&A

Accounting for Seasonal Working Capital Adjustments in M&A When a private business owner prepares to sell their company, they typically focus on negotiating the purchase price. However, in most private transactions, the final cash proceeds are adjusted based on the net working capital left in th

Accounting for Seasonal Working Capital Adjustments in M&A

When a private business owner prepares to sell their company, they typically focus on negotiating the purchase price. However, in most private transactions, the final cash proceeds are adjusted based on the net working capital left in the business at closing. Agreeing on a baseline target is a key step in these transactions. Proactively managing seasonal working capital adjustments is essential for transaction advisors. It prevents the seller from facing unexpected write-downs at closing.

In the transactional environment of 2026, seasonal working capital fluctuations are a frequent source of deal friction. Buyers attempt to set an artificially high target to force a purchase price reduction at closing. To protect the seller's proceeds and maintain negotiating momentum, M&A advisors must build a detailed working capital model before due diligence begins.

Free Resource: Try our working capital peg calculator to model monthly assets and liabilities and establish a defensible baseline for your transaction.

Why Seasonal Working Capital Adjustments Form a Major Diligence Focus

Boutique transaction teams in 2026 operate in a credit-constrained market where commercial lenders require clean balance sheets before approving acquisition financing. The Small Business Administration (SBA.gov) requires lenders to verify that a target company carries sufficient operating liquidity post-acquisition, making working capital a key factor in financing approval.

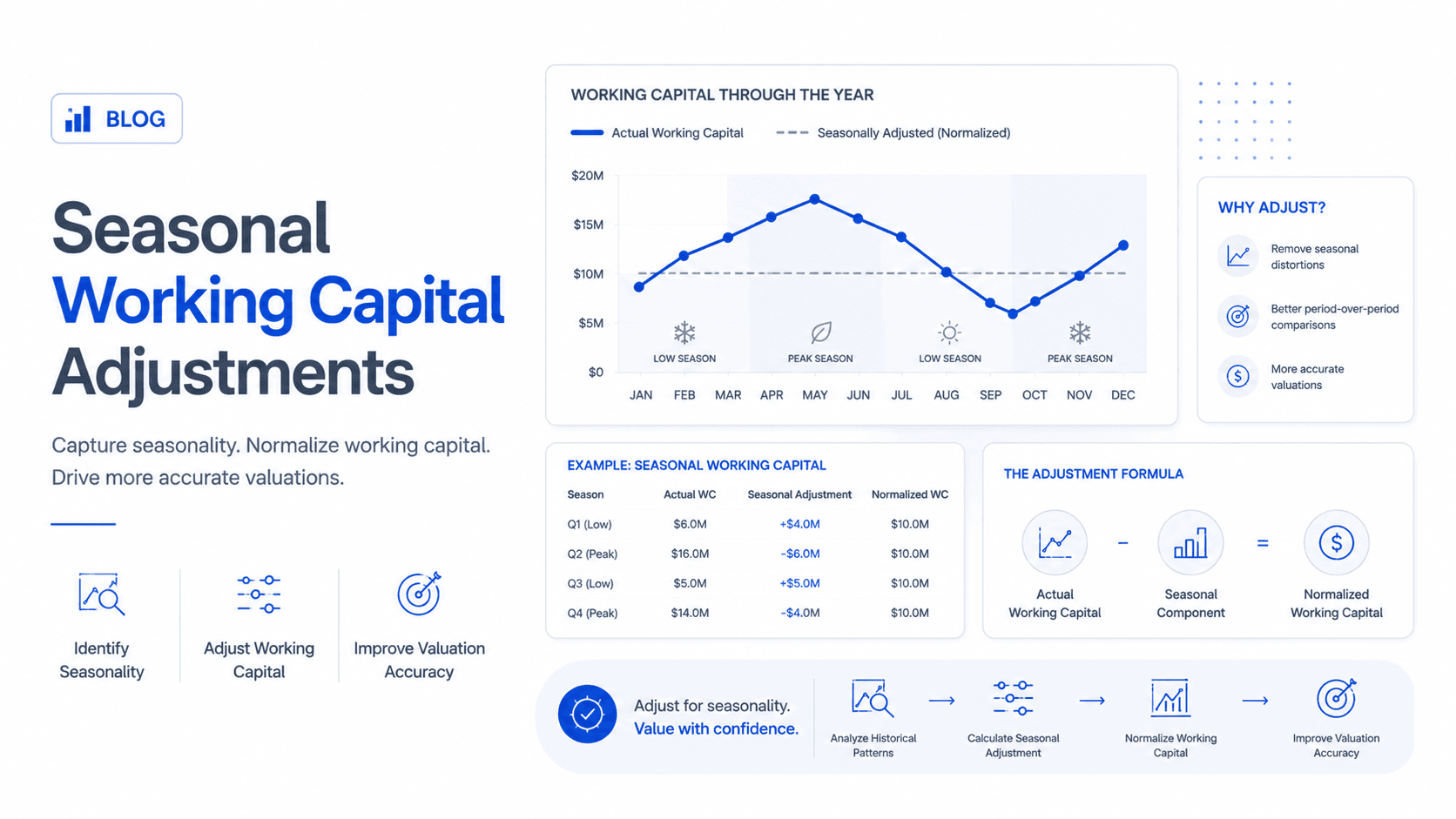

The challenge is that a company's working capital balance fluctuates based on monthly billing cycles, seasonal sales peaks, and inventory buildup. If a seller presents a P&L showing high operating income while the closing working capital falls below the peg due to standard seasonal purchasing patterns, buyers will adjust the purchase price. Seasonal working capital adjustments ensure that the peg represents a normalized average, preventing timing anomalies from affecting the final payout.

Case Studies: Seasonal Working Capital Errors That Cost Sellers Millions

Case Study: The Landscaper That Sold During Peak Operational Cycles

In one transaction involving a Midwest-based commercial landscaping provider, the owner signed an LOI with a purchase price of $6.0 million. The buyer proposed a static working capital target based on the company's December balance sheet, which represented the low-point of the company's operating cycle, with inventory and receivables at $450,000.

At closing, which occurred in June during peak operating season, the actual working capital rose to $1.1 million because the company carried high accounts receivable and inventory to support active projects. Under the unadjusted deal terms, the buyer kept this surplus without compensating the seller, essentially receiving $650,000 in free cash at closing. The seller closed the transaction with far less cash than anticipated, leading to significant dispute.

How It Should Be Done: Rolling 12-Month Adjusted Peg That Prevented a Closing Dispute

Conversely, a Southeast-based agricultural equipment distributor prepared for its sale by engaging an advisory team that conducted a comprehensive working capital audit. The advisors identified that the company's working capital fluctuated significantly throughout the year, peaking in spring and dropping in winter.

Using a professional working capital peg calculator, the advisors built a 12-month rolling average model, adjusting for one-time inventory fluctuations. They established a normalized working capital peg of $780,000. When the buyer proposed a static target based on the low-point month, the sell-side advisors presented their rolling average model. The buyer accepted the normalized peg, preventing a post-closing purchase price adjustment and securing the target valuation for the seller.

Managing Seasonal Working Capital Adjustments: A Step-by-Step Checklist for Sellers

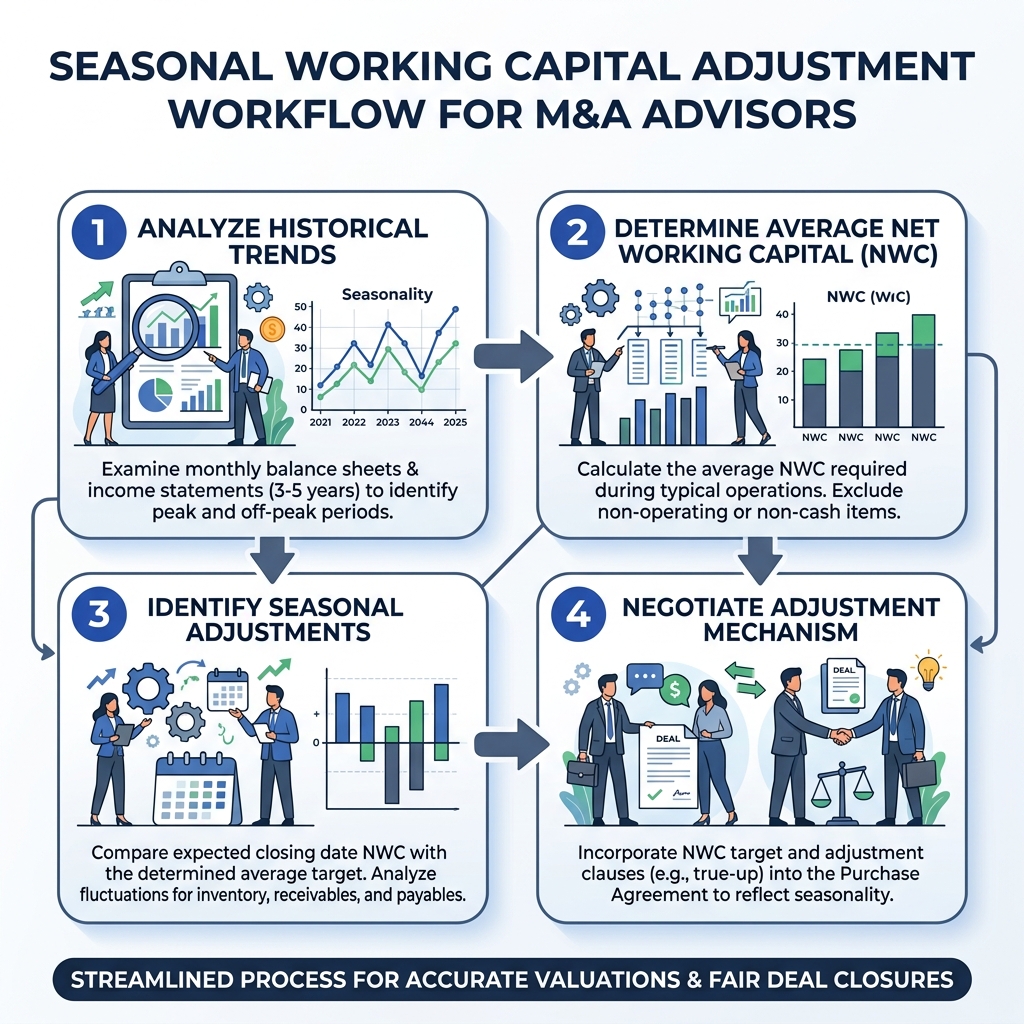

Transaction advisors must follow a structured approach to calculate and negotiate a defensible working capital baseline before launching marketing.

Phase 1: Reconciling Monthly Balance Sheets over a 24-Month Period

- Gather Historical Balance Sheets: Compile monthly balance sheets for the prior 24 months to trace seasonal cycles.

- Reconcile Accounts Receivable: Review the accounts receivable aging report, writing off uncollectible customer balances.

- Verify Accounts Payable: Reconcile outstanding vendor bills, ensuring all liabilities are recorded.

⚠️ Common Mistake: Calculating the peg based on a single month's balance sheet, ignoring seasonal operating requirements.

Phase 2: Identifying Seasonal Sales Peaks and Purchasing Lows

- Map Revenue Fluctuations: Identify months with high sales volume and trace corresponding increases in accounts receivable.

- Audit Inventory Cycles: Identify months with high inventory requirements to prepare for seasonal demand.

- Reference SEC Filing Standards: Review peer filing disclosures on SEC (SEC.gov) to compare standard seasonal adjustment definitions.

⚠️ Common Mistake: Assuming that seasonal fluctuations will not be analyzed by the buyer's Quality of Earnings team.

Phase 3: Building a Rolling Average Net Working Capital Baseline

- Calculate Monthly Working Capital: Apply the NWC formula for each month in the 24-month historical period.

- Exclude Non-Operating Items: Remove cash, interest-bearing debt, and tax assets from the working capital model.

- Apply Normalization Adjustments: Adjust for non-recurring events or deferred vendor payments.

⚠️ Common Mistake: Including cash in the net working capital calculation, violating the standard cash-free, debt-free transaction terms.

Phase 4: Constructing a Prioritized Working Capital Peg Proposal

- Build the Peg Bridge: Create a clear schedule displaying the monthly working capital calculations and adjustments.

- Draft the LOI Language: Ensure the LOI defines working capital using a detailed list of included and excluded accounts.

- Organize the Data Room: Upload the working capital model and general ledger detail to the virtual data room.

⚠️ Common Mistake: Leaving the definition of working capital ambiguous in the LOI, which gives the buyer leverage to define it during due diligence.

Peak Working Capital Target vs 12-Month Rolling Average: A Comparison

Understanding the structural differences between a peak target and a rolling average is key when negotiating working capital peg.

12-Month Rolling Average Method

- Calculation Basis: Calculated based on the average net working capital of the prior 12 monthly balance sheets.

- Seasonality Management: High; levels out seasonal fluctuations, protecting the seller during low-cash cycles.

- Valuation Fairness: Highly fair; represents the true average operating capital required to run the business.

- Buyer Acceptance: Standard practice in mid-market M&A, accepted by private equity and strategic acquirers.

Peak Month Target Method

- Calculation Basis: Calculated based on the month with the highest working capital requirements.

- Seasonality Management: Poor; forces the seller to leave excess cash in the business to meet the target at closing.

- Valuation Fairness: Unfair; overstates the average capital required to run operations, reducing seller proceeds.

- Buyer Acceptance: Often proposed by buyers to secure a purchase price reduction at closing.

How AIVI Streamlines Seasonal Working Capital Modeling for M&A Advisors

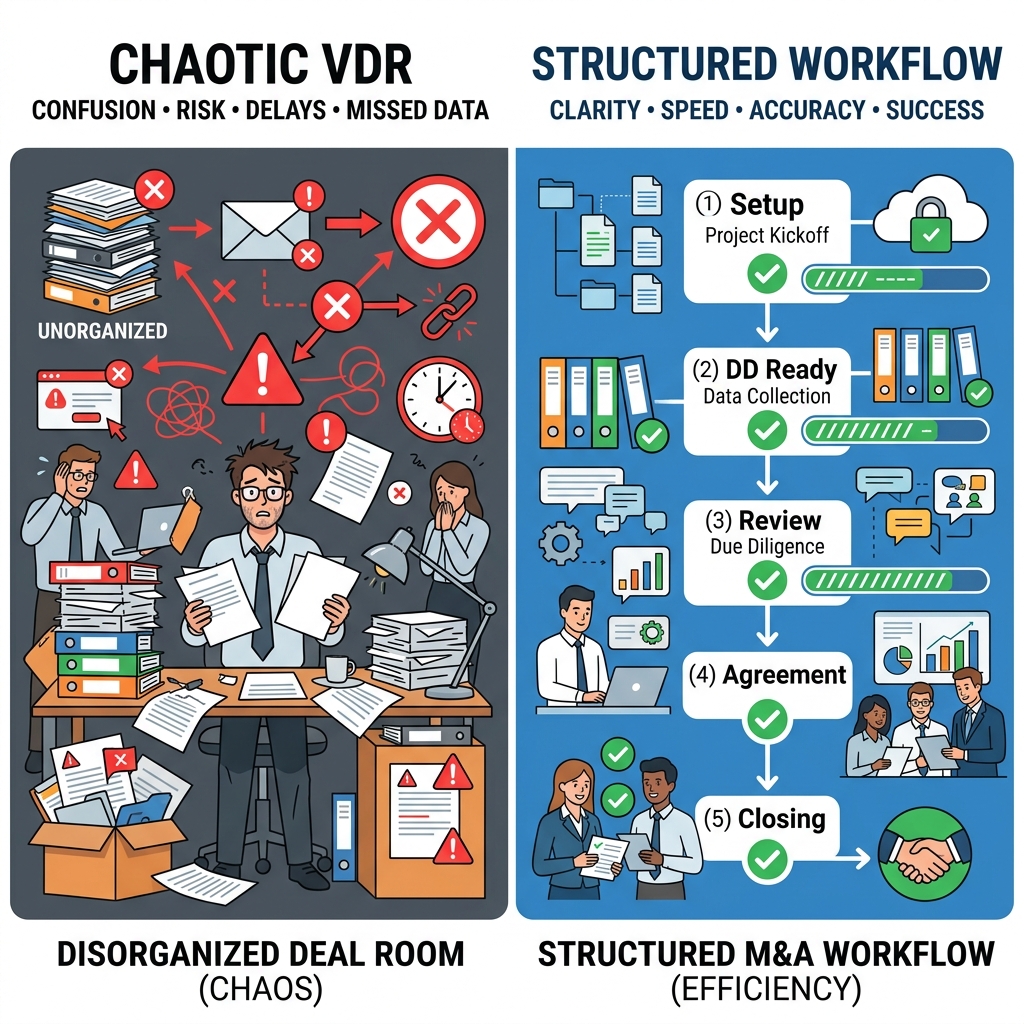

Analyzing working capital requirements requires reliable data organization. Sellers who rely on scattered files risk transaction delays. This is where modern transaction platforms are highly valuable.

By organizing balance sheets, tax filings, and general ledgers in a secure VDR remediation board, advisors can ensure that buy-side teams can audit the records efficiently.

Additionally, rather than manually building financial slides, advisors can use automated CIM generation tools to package the reconciliation models into a clear memorandum. Integrating transaction calculators with organized document management helps boutique firms maintain momentum.

Frequently Asked Questions

What are seasonal working capital adjustments in M&A?

Seasonal working capital adjustments are adjustments made to a company's working capital baseline during due diligence. The process involves calculating a rolling 12-month average of operating current assets and liabilities to level out seasonal fluctuations and establish a normalized target.

How does seasonal variance impact the net working capital peg?

Seasonal variance causes a company's working capital to fluctuate throughout the year. If a transaction closes during a peak season, the actual working capital will exceed the peg, requiring the buyer to pay the seller the surplus. If closing occurs during a low season, the working capital will fall below the peg, resulting in a purchase price reduction.

Why is a rolling 12-month average used to adjust for seasonality?

A rolling 12-month average is used because it represents the true average operating capital required to run the business over a full annual cycle. This levels out seasonal peaks and lows, protecting both parties from timing anomalies.

What happens if a transaction closes during the seller's peak season?

If a transaction closes during the seller's peak season, the actual working capital will exceed the target peg. Under standard deal terms, the buyer must pay the seller the surplus amount at closing, increasing the final proceeds.

How do you model seasonal cash flows using a working capital calculator?

To model seasonal cash flows, input monthly balance sheet data for the prior 12 to 24 months into a working capital calculator. The tool calculates the monthly net working capital, plots the seasonal cycle, and computes a normalized rolling average peg.

Disclaimer: The financial and legal information provided in this article does not, and is not intended to, constitute professional legal or financial advice; instead, all information, content, and materials available on this site are for general informational purposes only. Readers should contact their legal counsel or certified public accountant to obtain advice with respect to any particular transaction or regulatory matter.

Ready to automate M&A drafting & secure transaction readiness?

AIVI empowers boutique M&A firms and investment banks to generate CIMs, conduct instant VDR gap checks, and manage exit readiness automatically from a unified data model.