Leveraging Tech Integration Exit Readiness and Project Contract Reports

Leveraging Tech Integration Exit Readiness and Project Contract Reports It is early on a Tuesday morning in a midtown New York advisory office. The deal team is putting the final touches on exit materials for a high-growth IT system integrator. The company operates a regional network, claiming c

Leveraging Tech Integration Exit Readiness and Project Contract Reports

It is early on a Tuesday morning in a midtown New York advisory office. The deal team is putting the final touches on exit materials for a high-growth IT system integrator. The company operates a regional network, claiming consistent project flow and a massive active client contract base. However, the buyer's private equity diligence team has just requested a complete client contract retention register and a detailed project milestone audit. If the reports reveal that project milestones are delayed or that lead contracts lack active transfer covenants, the buyer's risk committee will enforce steep valuation discounts at close.

Advisors face massive operational friction when presenting tech integration exits without structured operational diagnostics. If client contracts and project registers are unorganized or lack supporting delivery records, buyers will assume that the business carries high near-term transition risks. Sell-side teams must implement structured project contract assessments to protect transaction multiples. By segmenting long-term contracts from temporary jobs, documenting client transfer covenants, and preparing clear contract schedules, advisors can defend the target valuation.

Free Resource: Model your exit readiness indicators and calculate your operational scores using our Exit Readiness Scorecard to align your tech metrics before buy-side audit teams review the registers.

Why Project Visibility and Client Covenants Have Become Critical in 2026

Boutique investment banks are handling complex transactions involving IT consultancies and system integration providers. Compliance guidelines from the Securities and Exchange Commission at SEC.gov enforce strict rules for commercial contract transfers and key personnel disclosures under FTC rules, making employee registers and project logs a primary target for diligence teams. Buy-side firms now use specialized auditing software to scan client registries and project histories, meaning that basic contract summaries are no longer sufficient. M&A advisors report that disputes over customer concentration and project milestone delays are a leading cause of price renegotiation during due diligence.

What we actually see in deals: transaction teams often rely on basic, unverified seller project logs when marketing the business. These summaries do not account for key employee dependencies, safety violations, or project scheduling overruns under current Federal guidelines. Buy-side groups exploit these vague lists to argue that the integrator’s project pipeline is dependent on the personal goodwill of the departing founder, requiring immediate price reductions. To defend transaction multiples, sell-side brokers must present the contracts as clean corporate assets, backed by verified transition protocols.

Case Studies: Loose Verbal Commitments vs. Reconciled Corporate Contracts

Case Study: The 35% Valuation Haircut on a Northeast Consultancy

A boutique advisory firm represented an IT consulting provider in the Northeast generating fifteen million dollars in annual revenue. The seller’s controller uploaded a list of active clients to the virtual data room without verifying that the primary accounts were documented under corporate contracts.

During due diligence, the buyer’s auditing team identified that several major clients had recently terminated their agreements, indicating high customer churn risk. Furthermore, two primary diagnostic leads—who generated thirty percent of total billing—lacked active post-closing employment covenants. The buyer used these operational gaps to claim that the business was unstable. The seller accepted a three million dollar discount and the deal was delayed by ninety days while the deal team audited the project registers.

How It Should Be Done: Securing a Premium Exit via a Reconciled Contract Audit

Conversely, a specialized M&A advisor represented a regional digital agency group. The advisor organized the transaction materials into a secure file workspace and established a structured exit readiness diagnostic workflow, linking every client agreement to a corporate entity.

The advisor utilized a secure advisory persona tuning process to build a detailed diagnostic index, highlighting that all core accounts had active multi-year terms with fixed pricing structures. The advisor managed document requests through a secure VDR Kanban workflow, sharing customer retention metrics instantly. A strategic buyer, realizing that the practice was fully compliant and the transition risk was negligible, submitted a cash offer at a premium multiple, closing the transaction on schedule without any price adjustments.

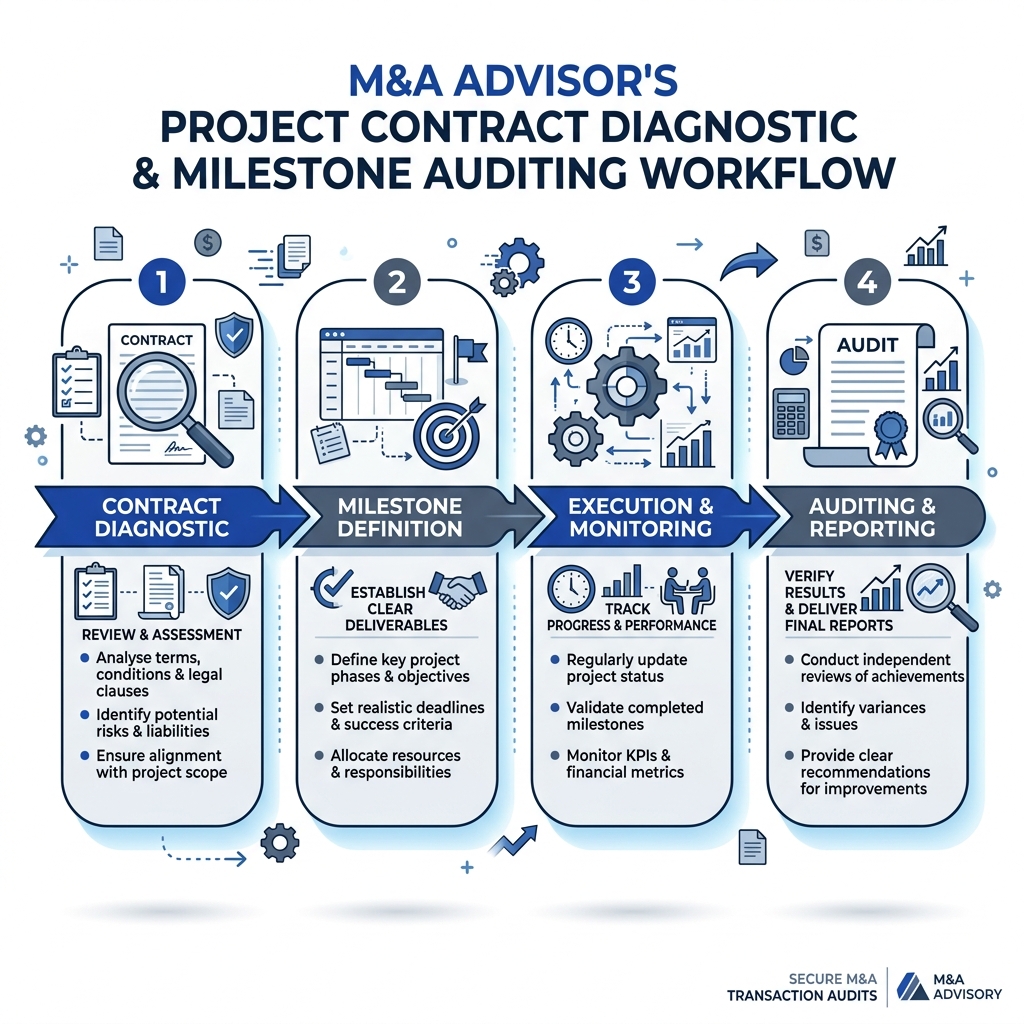

Auditing Tech Integration: Step-by-Step Checklist for M&A Deal Teams

Phase 1: Conducting the Project Contract and Milestone Audit

- Verify Buyer Entity Details: Review buyer profiles at SBA.gov to confirm transaction entities before sharing proprietary store credentials.

- Review Project Milestone Progress: Audit project management software to calculate the historical completion rate.

- Verify Contract Transfer Covenants: Confirm that all client contracts contain active transfer or change-of-control provisions.

- Audit Project Billing Accuracy: Reconcile project billing records against actual delivery milestones.

⚠️ Common Mistake: Sharing unredacted employee compensation details before the buyer has submitted a verified Quality of Earnings plan.

Phase 2: Restructuring and Transferring Client Relationships

- Calculate Client Retention Rates: Document the percentage of clients who renew agreements annually.

- Segment Revenue by Account: Chart client distribution to prove that no single account represents more than fifteen percent of revenue.

- Audit New Account Sources: Highlight that client acquisition channels belong to the company brand, not individuals.

- Establish transition Timelines: Map out the schedule of client transition to project managers to show business stability.

Phase 3: Mitigating Key Engineer and Labor Risks

- Verify Post-Closing Employment Contracts: Audit all lead engineer agreements to ensure they extend at least twelve to twenty-four months.

- Review Non-Compete Agreements: Confirm that geographical non-compete covenants are signed and compliant with local laws.

- Calculate Wage Rate Escalations: Detail historical wage adjustments to prove that clinical labor costs are stable.

- Establish Employee Incentive Plans: Reconcile active employee incentive plans and stock options on the balance sheet.

⚠️ Common Mistake: Sharing proprietary bidding estimators before securing a binding letter of intent from the buyer.

Phase 4: Presenting the Tech Integration Readiness Report

- Format the Segmented Sourcing Table: Present active customer profiles, monthly visitors, and billing metrics in the CIM.

- Draft the Operating Narrative: Describe how the company's task management software minimizes scheduling overruns.

- Include Key Man Covenants: Display active key employee agreements and retention terms to prove clinical stability.

- Export Clean PDF Files: Remove editor names and historical draft metadata from all project schedules before distribution.

Loose Verbal Commitments vs. Reconciled Corporate Contracts: A Comparison

Tech integration advisors must evaluate the strategic differences between legacy verbal commitments and reconciled corporate contracts.

Reconciled Corporate Contracts

- Valuation Multiple: High; institutional acquirers recognize the visibility of clean, active project assets.

- Deal Leverage: High; demonstrates that future operations will support post-close capacity.

- Onboarding Speed: Fast; provides complete corporate registrations to speed up due diligence.

- Buyer Risk: Low; reduces the opportunity for buy-side groups to claim client transition risk.

Loose Verbal Commitments

- Valuation Multiple: Low; reflects high risk of customer cancellations and developer departures.

- Deal Leverage: Poor; allows the buyer to argue that the client relationships are unstable.

- Onboarding Speed: Slow; requires manual auditing of personal bills and shipping invoices during due diligence.

- Buyer Risk: High; invites buy-side auditors to demand price adjustments.

Driving Tech Services Deal Value via AIVI Automation

Boutique M&A advisors use the AIVI platform to manage folder permissions and secure sensitive contract records. Teams use AIVI's VDR Kanban workflow to separate documents into security tiers, ensuring that only verified buyers can access sensitive employee agreements and customer databases.

Advisors also utilize AIVI's advisory persona tuning to compile consistent transaction books. This integration ensures that the platform ownership schedules in marketing teasers align with the records stored in the secure data room, reducing buy-side opportunities to renegotiate pricing due to mismatched information.

Frequently Asked Questions

What is a tech integration exit readiness project contracts report?

A project contracts report is an audit of an IT system integrator's client contracts, project delivery milestones, key engineer covenants, and client concentration.

How do advisors calculate working capital targets for system integrator exits?

Advisors model historical monthly billing cycles, cash requirements, and receivables to establish a realistic peg for closing.

Why do buyers discount tech integrators operating with founder dependencies?

Founder dependencies increase operational risk, as the loss of the founder post-close can quickly drop client volume and project delivery.

Can an exit readiness scorecard assist in sizing project contract risks?

Yes. Modeling project milestones helps advisors prove the actual capital efficiency of the business, protecting the target valuation.

What compliance standards apply to employee incentive plans under IRS rules?

IRS rules require strict documentation of valuation models, vesting schedules, and tax withholding for all employee stock grants.

Disclaimer: The financial and legal information provided in this article does not, and is not intended to, constitute professional legal or financial advice; instead, all information, content, and materials available on this site are for general informational purposes only. Readers should contact their legal counsel or certified public accountant to obtain advice with respect to any particular transaction or regulatory matter.

Ready to automate M&A drafting & secure transaction readiness?

AIVI empowers boutique M&A firms and investment banks to generate CIMs, conduct instant VDR gap checks, and manage exit readiness automatically from a unified data model.