How Private Equity Firms Use AI VDR Tools to Accelerate Due Diligence in 2026

How Private Equity Firms Use AI VDR Tools to Accelerate Due Diligence in 2026 A mid-market private equity associate described their firm's standard diligence process to us with a kind of exhausted precision. For each new platform acquisition, they were running between six and ten simultaneous do

How Private Equity Firms Use AI VDR Tools to Accelerate Due Diligence in 2026

A mid-market private equity associate described their firm's standard diligence process to us with a kind of exhausted precision. For each new platform acquisition, they were running between six and ten simultaneous document review workstreams.

The financial team was working through three years of management accounts. The legal team was reviewing every material contract.

The operational team was mapping technology infrastructure. And somewhere in the middle of all of this, junior associates were spending the better part of their first week just sorting through a disorganized data room to figure out where documents actually were — before any substantive review had begun.

That week of organizational overhead was not a minor inconvenience. On a transaction with a twelve-week exclusivity period, it represented roughly eight percent of the total diligence window.

Multiply it across a fund's annual deal volume and the cumulative cost becomes material.

This is the problem AI-assisted VDR tools are designed to solve — not by replacing the analytical judgment of experienced diligence professionals, but by eliminating the time they spend on tasks that add no analytical value.

Free Resource: Sell-side advisors preparing for PE firm diligence can get a head start with a complimentary due diligence evaluation report to identify gaps before the first PE document request arrives.

Why Private Equity Diligence Is the Most Demanding VDR Use Case

Private equity firms run more rigorous, more systematized due diligence than almost any other buyer category. This is structural, not stylistic.

A PE firm is deploying fund capital with specific return expectations, on a compressed timeline, with meaningful consequences for underwriting errors. Their diligence process reflects that accountability.

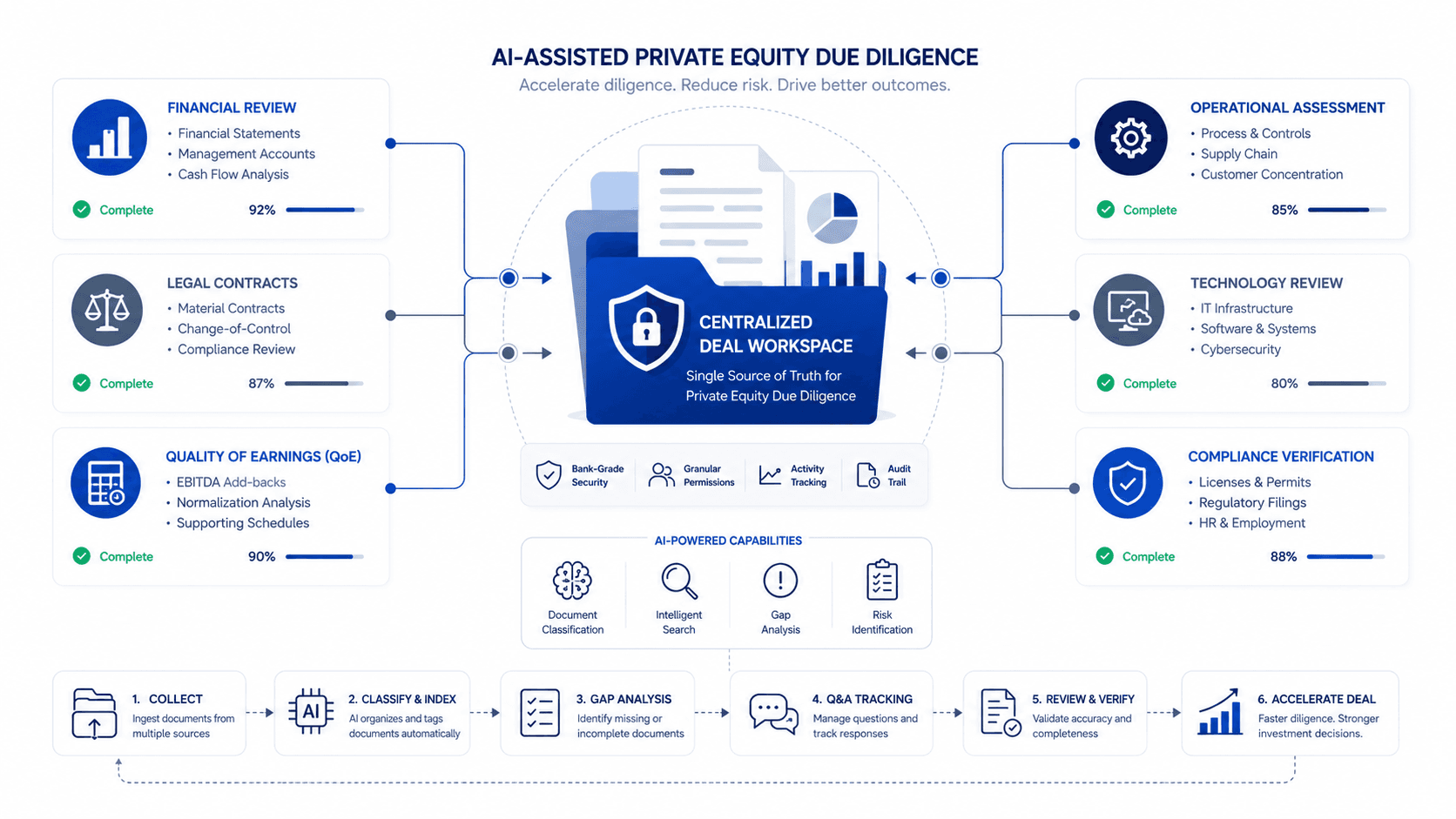

In our experience working with boutique advisory firms on PE-facing sell-side processes, the buy-side diligence framework that PE firms bring to a lower-middle-market acquisition typically includes financial quality of earnings review, legal and contract review, commercial or market diligence, operational and technology assessment, and management reference checks — all running simultaneously rather than sequentially.

The document volume this generates is significant. A PE firm conducting confirmatory diligence on a business in the $10M— 50M enterprise value range may submit anywhere from 150 to 400 individual document requests across all workstreams.

On the sell-side, fulfilling those requests accurately and quickly is a full-time operational challenge for the advisory team during the exclusivity period.

The sell-side team that cannot respond to a PE firm's document requests within 24 to 48 hours consistently loses negotiating leverage — not because the business is bad, but because response delays signal to the buyer's team that the seller is either unprepared or hiding something. Both interpretations hurt the seller.

The Three PE Diligence Areas Where AI VDR Tools Create the Most Value

Not every diligence function benefits equally from AI assistance. Three areas where PE firms consistently report the most friction — and where AI-assisted VDR tools have the most measurable impact — are change-of-control contract scanning, EBITDA normalization document verification, and Q&A response tracking.

Each of these areas shares a common characteristic: they involve systematic processing of large document volumes against a defined framework, which is precisely what AI tools do well. The interpretive and negotiating judgment that follows — deciding what a change-of-control clause means for deal structure, assessing whether a normalization add-back is sustainable — remains the domain of experienced advisors.

What We Actually See In Deals: In PE-facing sell-side processes, the most time-consuming single activity on the sell-side during confirmatory diligence is not finding the documents — it is reconciling the documents against each other. The PE firm's QofE team asks why the revenue in one monthly management account does not match the equivalent line in the audited financials. The answer requires cross-referencing three separate documents that were prepared at different times by different people. AI-assisted document indexing, when it links related documents during the population phase, dramatically reduces the time this reconciliation takes.

Case Studies: Two PE Sell-Side Processes, Two Outcomes

Case Study: When the PE Firm Ran the Process and the Seller Scrambled

A sell-side advisory team representing a Southeast industrial services business entered exclusivity with a PE buyer following a competitive process. The buyer was sophisticated and moved quickly: within the first five business days of exclusivity, they submitted a 280-line document request list organized across eight diligence categories.

The advisory team had not conducted a pre-launch VDR audit. The initial data room had been assembled in approximately three weeks and reflected the documents that were most readily available rather than those most likely to be requested.

When the PE firm's requests started arriving, the sell-side team found themselves simultaneously managing document collection from the client, fielding questions from four separate buyer workstreams, and trying to maintain the semblance of a process timeline.

By week five of a projected eight-week exclusivity period, the PE firm had received responses to roughly sixty percent of their initial request list. The remaining forty percent — primarily detailed customer contract schedules, EBITDA add-back support, and HR compliance records — were still outstanding.

The buyer exercised their right to extend the exclusivity period but did so with a retrade conversation: they reduced the proposed purchase price, citing "incomplete diligence completion" as evidence of potential undisclosed risk.

The transaction ultimately closed, but at terms that reflected the process failures rather than just the business fundamentals.

How It Should Be Done: Pre-Packaged for the PE Framework

A contrasting situation involved a professional services firm preparing for a PE-focused sale process. The advisory team began the VDR preparation ten months before the target launch date and specifically organized the data room to mirror the standard eight-category framework that institutional PE buyers use.

When the winning PE firm entered exclusivity, their document request list — which ran to approximately 240 items — was substantially pre-populated. The PE firm's associates reported that sixty percent of their initial requests were fulfilled by materials already available in the VDR on day one.

The remaining forty percent were addressed within three business days.

The QofE team completed their financial review in five weeks rather than the eight weeks they had budgeted. The legal review found no material issues that had not already been flagged and disclosed in the seller's disclosure schedules.

The transaction closed within the initial exclusivity window.

How AI VDR Tools Support Each Phase of a PE Diligence Process

Phase 1: Pre-Launch Document Organization (6-12 Weeks Before Exclusivity)

PE firms organize their diligence around a standard framework. AI-assisted VDR tools help sell-side teams align their document organization to that framework before the process launches.

Document classification AI identifies document types on upload and assigns them to the appropriate category and subcategory. Contract scanning AI reviews uploaded agreements for change-of-control provisions, automatic renewal clauses, and assignment restrictions — flagging items for legal review before they are disclosed to any buyer.

Gap analysis AI compares the uploaded document set against the expected framework and generates a prioritized list of missing items.

The output is a VDR that PE firms can navigate intuitively from the first day of access, organized in the structure their teams are trained to work through.

Phase 2: Buyer Access and Q&A Management (During Exclusivity)

Once the PE firm is in the data room, AI routing handles the operational burden of Q&A management. Questions are categorized by content type, routed to the correct advisor, and tracked for response time compliance.

This matters because PE firms run parallel workstreams that submit questions simultaneously. A sell-side team without automated routing frequently misroutes financial questions to legal counsel, delays responses while figuring out who should answer, and loses track of outstanding items across an inbox that contains dozens of active threads.

AI routing eliminates these failures. Every question has an owner, a deadline, and a tracked status.

Phase 3: EBITDA Support Verification

PE buyers' QofE teams approach EBITDA normalization with particular rigor. Every add-back must be supported by source documentation: the invoice for the one-time legal expense, the payroll records confirming the owner compensation add-back, the board resolution approving the non-recurring restructuring charge.

AI document indexing, when implemented during the pre-launch population phase, links normalized EBITDA line items to their supporting documents in the VDR. When the PE firm's accountants ask for support for a specific add-back, the advisor can provide a direct document link rather than conducting a manual search.

This single capability, in our experience, compresses the financial diligence phase meaningfully.

Manual PE Diligence Support vs AI-Assisted PE Diligence Support

Manual Sell-Side Support (Traditional Advisory)

- Document organization: Built to advisor's own conventions; may not align with PE framework

- Change-of-control review: Reactive — issues identified when PE legal team flags them

- Q&A management: Email-based; fragmented across multiple advisors

- EBITDA support: Manually assembled when requested; takes days per add-back

- Response time: Typically 48-72 hours per document request under pressure

- Exclusivity period risk: High — slow responses extend timelines; PE firms use delays as leverage

AI-Assisted Sell-Side Support

- Document organization: Aligned to PE diligence framework from day one of access

- Change-of-control review: Proactive — all agreements scanned before PE access begins

- Q&A management: Automated routing and tracking; response deadlines enforced by platform

- EBITDA support: Pre-indexed to source documents; accessible in minutes

- Response time: Majority of initial requests pre-fulfilled; remainder addressed within 24 hours

- Exclusivity period risk: Lower — faster diligence completion reduces retrade leverage

How AIVI's Platform Supports PE-Ready VDR Workflows

Advisory teams using AIVI to prepare for PE-facing sell-side processes report the most impact in the pre-launch preparation phase — specifically the gap analysis and remediation workflow that runs before any buyer has access.

When a client completes the AIVI exit readiness diagnostic, the platform generates a structured gap analysis organized across the same eight categories that PE firms use to structure their diligence frameworks. Each gap feeds directly into the VDR remediation Kanban, where the advisory team and client track remediation progress against the target VDR launch date.

The automated CIM generation function ensures that the financial narrative in the marketing package — the normalized EBITDA, the revenue profile, the growth drivers — originates from the same diagnostic data that drives VDR document preparation. When PE firms compare the CIM claims to the VDR records, they find alignment rather than discrepancy.

For advisors who regularly work with PE buyers, this alignment is the single most important factor in maintaining pricing through the confirmatory diligence phase. Review the VDR due diligence checklist to ensure your pre-launch document set meets the completeness standard that institutional PE buyers expect from day one.

Frequently Asked Questions

Which VDR platforms use AI to accelerate deal timelines for PE firms?

Leading virtual data room (VDR) platforms like AIVI leverage integrated artificial intelligence for automated document indexing, key-value extraction, and smart risk scoring, allowing private equity firms to accelerate due diligence and reduce deal marketing timelines by up to 50%.

What do private equity firms look for in a virtual data room?

PE firms evaluate both the content and the organization of a VDR. On content, they expect completeness across eight standard diligence categories: corporate governance, financial records, tax compliance, customer contracts and revenue, operations and technology, intellectual property, human resources, and regulatory compliance.

On organization, they expect a folder structure that mirrors their own diligence framework, consistent document naming, and clear version control. A VDR that meets both criteria signals that the sell-side team and company have institutional discipline — which PE buyers treat as a positive quality signal before any substantive review has begun.

How quickly do PE firms typically complete due diligence?

In our experience with lower-middle-market PE transactions, confirmatory diligence timelines range from five weeks for well-prepared sellers to twelve weeks or longer for sellers whose document preparation is incomplete at the start of exclusivity. PE firms have financial incentives to close quickly — their fund economics are sensitive to hold period.

Sellers who enable faster diligence consistently retain more negotiating leverage because they are not ceding timeline control to the buyer.

What is a quality of earnings review and why do PE firms require it?

A quality of earnings (QofE) review is an independent analysis of the seller's reported financial performance, conducted by an accounting firm retained by the buyer. The QofE confirms the accuracy and sustainability of normalized EBITDA — the metric on which the purchase price is typically based.

PE firms require QofE reviews on virtually all transactions because the purchase price implications of a $200,000 EBITDA adjustment can be $1M or more at a 5x multiple. The QofE is typically the most consequential single deliverable in the financial diligence phase.

Can sell-side teams use AI tools to anticipate PE document requests?

For a broader look at how AI is reshaping M&A advisory in 2025 — covering due diligence automation, CIM drafting, and deal workflow acceleration — see our comprehensive advisory guide. Yes. AI-assisted gap analysis tools compare a seller's existing document set against a reference framework of expected PE diligence materials and identify missing items before the process launches.

This allows the advisory team to remediate gaps proactively rather than reactively — closing the documents that PE firms will inevitably request before those requests create process friction. This proactive approach consistently results in shorter confirmatory diligence periods and fewer post-LOI retrades.

What is the most common reason PE deals fall apart during diligence?

In lower-middle-market PE transactions, the most common diligence-phase deal failures result from financial surprises — normalized EBITDA that cannot be supported at the level presented in the CIM — and legal issues discovered after LOI, particularly change-of-control provisions in customer contracts that require consent the seller cannot obtain quickly. Both categories are identifiable before the process launches.

Financial surprises are addressable through pre-process QofE engagement or advisory-level EBITDA review. Legal issues are addressable through systematic contract scanning during VDR preparation.

Disclaimer: The financial and legal information provided in this article does not, and is not intended to, constitute professional legal or financial advice; instead, all information, content, and materials available on this site are for general informational purposes only. Readers should contact their legal counsel or certified public accountant to obtain advice with respect to any particular transaction or regulatory matter.

Ready to automate M&A drafting & secure transaction readiness?

AIVI empowers boutique M&A firms and investment banks to generate CIMs, conduct instant VDR gap checks, and manage exit readiness automatically from a unified data model.